WANT THIS ISSUE?

Download your own personal copy of this issue in PDF format. Click the button below:

WANT THIS ISSUE?

Download your own personal copy of this issue in PDF format. Click the button below:

Former first lady Rosalynn Carter was a caregiver herself and she believed that family caregiving is a cycle of life that touches everyone. In this issue, four people, each at a different point on the cycle, share their care stories from the heart, offering words of wisdom and points of caution. As you read, consider…

If I were to open a crime college, a place to learn the fine art of thievery, one class that would assuredly be on the curriculum would be Advance Fee Frauds, commonly known as sweepstakes and lottery frauds. This con involves the victim being told the lie that money is coming their way (usually from lottery winnings, insurance refunds or inheritance) but a fee/tax/processing charge has to be paid first to receive it. This one scheme is responsible for more money being stolen in Hawai‘i than any other crime.

According to the Better Business Bureau, nearly 500,000 people have reported this fraud to various enforcement agencies in North America from 2015 to 2017. In that time, funds lost totaled $344,414,685. However, studies have shown only 1 in 25 cases are even reported to the police.

These scams tend to originate outside of the U.S., mainly in countries such as Jamaica and Costa Rica. Losses to fraud in Jamaica in 2015 (those that had been discovered) amounted to over $38 million. Money that resulted from these scams has been used to buy guns and drugs within Jamaica. In fact, so much money is being made in Jamaica from this scam, that organized crime has dramatically increased, resulting in deadly gang wars between rival fraud groups spilling out onto the streets. As a result of these problems, a State of Emergency has been declared for Jamaica.

These scams tend to originate outside of the U.S., mainly in countries such as Jamaica and Costa Rica. Losses to fraud in Jamaica in 2015 (those that had been discovered) amounted to over $38 million. Money that resulted from these scams has been used to buy guns and drugs within Jamaica. In fact, so much money is being made in Jamaica from this scam, that organized crime has dramatically increased, resulting in deadly gang wars between rival fraud groups spilling out onto the streets. As a result of these problems, a State of Emergency has been declared for Jamaica.

Countries such as Jamaica and Costa Rica both have large English-speaking populations, which is effective when speaking to potential victims. They claim they are from somewhere within the U.S., giving a false sense of security to victims, and slowly convince them they are not being scammed.

Costa Ricans tend to use Voice Over Internet Protocol (VOIP), also known as internet phones, which give them the ability to change their area code. They often claim to be from a government agency to give potential victims a false sense of security when providing payment for taxes, fees, transportation, and/or security, for their “winnings.”

Operations in Canada, Israel, Spain, and the Philippines have been linked to these sweepstakes/lottery scams, too. They tend to “spoof” phone numbers, resulting in area codes that appear to come from within the U.S. — Las Vegas or Washington D.C. area codes are often used.

The takeaway from all this is people need to realize that there is no “free lunch” and they are not lucky enough to get something for nothing. As I explained in the Oct/Nov 2017 and Dec/Jan 2018 issues (online at www.generations808.com under “Wisdoms”), a person in Hawai‘i has a ZERO percent chance of winning the lottery. Too many people have fallen victim to this scam and have fueled crime and violence all over the world.

To report suspected elder abuse, contact the Elder Abuse Unit at 808-768-7536 | ElderAbuse@honolulu.gov

If I were to open a crime college, a place to learn the fine art of thievery, one class that would assuredly be on the curriculum would be Advance Fee Frauds, commonly known as sweepstakes and lottery frauds. This con involves the victim being told the lie that money is coming their way (usually from…

It is not just families who disagree about the interpretation of legal documents. There seems to be tension among estate planning attorneys in regard to recommending that clients write down their heartfelt intentions to accompany those documents. Many lawyers believe that it is the form that is most important — that the written legal language will communicate their client’s heartfelt wishes. Others believe that, no matter how carefully written, the form alone cannot transfer intention.

This is particularly true of discretionary trusts. Although the Trust provides the legal power for the Trustee to act, it usually does not state the maker’s underlying reasoning or intention of how the client would like to see their assets spent.

In his book Borrowed Narratives, Harold Smith tells us that making the personal statement in story form is better remembered and more persuasive than a sterile legal document. He further states that putting one’s thoughts in writing slows it down for the reader so that they can better understand the maker’s meaning.

Please make sure, when you are working with your estate planning attorney, that your underlying intentions for making the trust are clearly defined. This can make all the difference.

Stephen B. Yim, Attorney at Law

2054 S. Beretania St., Honolulu HI 96826

808-524-0251 | www.stephenyimestateplanning.com

It is not just families who disagree about the interpretation of legal documents. There seems to be tension among estate planning attorneys in regard to recommending that clients write down their heartfelt intentions to accompany those documents. Many lawyers believe that it is the form that is most important — that the written legal language will communicate…

Many parents, in addition to planning for their own future, care deeply about helping their children find their financial footing as they enter adulthood. Having spent decades building up their nest eggs for retirement, they recognize the power of long-term financial planning and hope their children will capture the same benefits by starting to invest while they are young. Convincing someone just starting off in their careers to set aside money for retirement — which to them, may seem like light years away — can be a tough sell. But, initiating the conversation in a respectful and educated manner may eventually compel them to make it a priority. If you’re a parent looking for guidance in this area, consider the following discussion pointers.

First, recognize the challenges young professionals may face

Those starting their career often face two challenges in establishing their nest egg. The first is feeling that they have all the time in the world to save for retirement. The second challenge is that young adults are balancing numerous priorities with their newfound financial independence. Acknowledge and be realistic about these hurdles, even as you make the case for setting aside money for retirement.

Then, outline the key reasons for making retirement savings a priority

If you or your child would like assistance crafting a retirement saving strategy, reach out to a financial advisor. Together you can find a way to balance the items most important to you.

MICHAEL W. K. YEE, CFP

1585 Kapiolani Blvd., Suite 1100 Honolulu, HI 96814

808-952-1222, ext. 1240 | michael.w.yee@ampf.com

Michael W. K. Yee, CFP®, CFS®, CLTC, CRPC ®, is a Private Wealth Advisor, Certified Financial Planner ™ practitioner with Ameriprise Financial Services, Inc. in Honolulu, HI. He specializes in fee-based financial planning and asset management strategies and has been in practice for 31 years.

Investment advisory products and services are made available through Ameriprise Financial Services, Inc., a registered investment adviser.

Ameriprise Financial Services, Inc. Member FINRA and SIPC.

© 2018 Ameriprise Financial, Inc. All rights reserved. File # 2171757

Many parents, in addition to planning for their own future, care deeply about helping their children find their financial footing as they enter adulthood. Having spent decades building up their nest eggs for retirement, they recognize the power of long-term financial planning and hope their children will capture the same benefits by starting to invest…

When hiring a caregiver, you may be tempted to try to make the process as simple as possible by treating the caregiver as a “private contractor.” You tell the person “I will pay you so much an hour, and you deal with the IRS and the State when it comes time to pay taxes.” After all, taking on the responsibilities of withholding taxes (and then paying the taxing authorities), buying Workers’ Compensation insurance, paying Social Security and Medicare tax, and all the rest, can be a real pain. However, the IRS and the State will take the position that the caregiver is an “employee,” that you are an “employer,” and that all the legal obligations that attach to those labels are applicable to your situation.

When hiring a caregiver, you may be tempted to try to make the process as simple as possible by treating the caregiver as a “private contractor.” You tell the person “I will pay you so much an hour, and you deal with the IRS and the State when it comes time to pay taxes.” After all, taking on the responsibilities of withholding taxes (and then paying the taxing authorities), buying Workers’ Compensation insurance, paying Social Security and Medicare tax, and all the rest, can be a real pain. However, the IRS and the State will take the position that the caregiver is an “employee,” that you are an “employer,” and that all the legal obligations that attach to those labels are applicable to your situation.

IRS Publication 926 gives very helpful guidance to those hiring household employees, including caregivers. Go through that publication, which can be found at https://www.irs.gov/forms-pubs/about-publication-926, and consider all the questions it poses, several of which might surprise you. For example, can your prospective caregiver legally work in the U.S.? How do you verify that, and what records must you keep to prove that you satisfied your obligation to verify the caregiver’s status? You can find all the resources and forms you will need for that on the U.S. Citizenship and Immigration Services website www.uscis.gov/i-9-central or call 800-375-5283.

Depending on your budget, it may make sense to look into local employment or caregiver agencies. This simplifies your job, because you can contract with the agency, and the agency will be the caregiver’s employer and will deal with all of the details of being an employer. You will pay a premium for this kind of service, but the agency’s experience and employment expertise may make the extra cost seem like a bargain.

Another set of issues arises if you opt to be the employer of a caregiver, and then your employee is injured on the job. If you have made sure to carry the right kinds of insurance, you will be fine. However, the consequences of failing to do so can be financially disastrous. An agency will probably carry Workers’ Compensation insurance, but you should be sure to talk with your personal insurance professional to find out if there is anything else you should do to protect yourself through your homeowner’s and umbrella policies.

The bottom line is that you should never hire a caregiver without carefully considering your legal responsibilities and potential liabilities, and making sure they are addressed. Ask your trusted advisors — your CPA, your lawyer, and your insurance professional — for guidance, and check out the resources cited above. You will be glad you did.

SCOTT MAKUAKANE, Counselor at Law

Focusing exclusively on estate planning and trust law.

www.est8planning.com

808-587-8227 | maku@est8planning.com

When hiring a caregiver, you may be tempted to try to make the process as simple as possible by treating the caregiver as a “private contractor.” You tell the person “I will pay you so much an hour, and you deal with the IRS and the State when it comes time to pay taxes.” After…

One question that is frequently asked by people about to turn 65 who have health insurance through an employer is:

“Do I need to enroll in Medicare?”

Good question! If you or your spouse are still working when you turn age 65 and have insurance through your employer you may consider delaying Medicare Part A and Part B until you retire if you have Creditable Coverage, which means coverage as good as Medicare.

Or you can choose to elect your Part A, which is premium-free, and delay Part B until retirement. Depending on the size of the group, one plan would be primary while the other would be secondary.

Or you can choose to elect your Part A, which is premium-free, and delay Part B until retirement. Depending on the size of the group, one plan would be primary while the other would be secondary.

The first step is to contact your (or your spouse’s) HR Department to make sure that your current coverage is creditable and find out how it will work with Medicare before you make your decision. When coverage through your employer ends you will be provided with a Special Enrollment Period that lasts for eight months, in which you will want to sign up for Medicare so you will not incur a penalty.

Another step you might want to take is to contact a licensed, experienced agent to assist you in researching the Medicare Advantage Plans, Medicare Supplement Insurance and Prescription Drug Plans that are available in your area.

COPELAND INSURANCE GROUP

1360 S. Beretania St., Suite 209, Honolulu HI 96814

808-591-4877 | margaret@copelandgroupusa.

One question that is frequently asked by people about to turn 65 who have health insurance through an employer is: “Do I need to enroll in Medicare?” Good question! If you or your spouse are still working when you turn age 65 and have insurance through your employer you may consider delaying Medicare Part A…

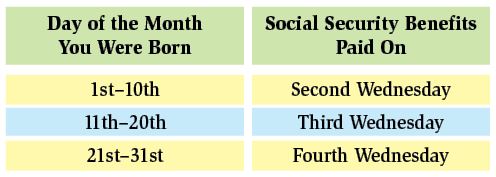

Social Security benefits are paid each month. Generally, new retirees receive their benefits on either the second, third, or fourth Wednesday of each month, depending on the day in the month the retiree was born. In general, here’s how we assign payment dates:

Social Security benefits are paid each month. Generally, new retirees receive their benefits on either the second, third, or fourth Wednesday of each month, depending on the day in the month the retiree was born. In general, here’s how we assign payment dates:

There are exceptions. For example, children and spouses who receive benefits based on someone else’s work record will be paid on the same day

There are exceptions. For example, children and spouses who receive benefits based on someone else’s work record will be paid on the same day

as the primary beneficiary.

For others, we may issue your payments on the 3rd of each month. Among other reasons, we use that payment date if:

✓ you filed for benefits before May 1, 1997;

✓ you also receive a Supplemental Security

Income (SSI) payment; or

✓ your Medicare premiums are paid for by the state where you live.

Those receiving SSI payments due to disability, age, or blindness are paid on the 1st of each month.

If your payment date falls on a federal holiday or weekend, expect to receive that month’s payment on the weekday immediately prior.

An easy-to-read schedule can be found at

www.ssa.gov/pubs/EN-05-10031-2018.pdf

For questions, online applications or to make an appointment to visit a SSA office, call from 7am–5pm, Mon–Fri: 800-772-1213 (toll free) | www.socialsecurity.gov

Social Security benefits are paid each month. Generally, new retirees receive their benefits on either the second, third, or fourth Wednesday of each month, depending on the day in the month the retiree was born.

Volunteering is a popular antidote to feelings of isolation that can occur as we age. Here are two programs that enable seniors to share their time and skills with younger generations.

Encore: Gen2Gen

Encore: Gen2Gen

Child and Family Service (CFS) has served the needs of vulnerable populations in Hawai‘i since 1899. In partnership with a national nonprofit, Encore, CFS offers many ways for volunteers aged 50+to support that important work.

Volunteer coordinator, Encore Fellow Kevin Henry, can find a place for you no matter if you have only a few hours a month or if you feel you don’t have any special skills. Doing inventory at a donation center or mentoring about financial literacy are just two examples.

Foster Grandparent Program

Foster Grandparent Program

If you are aged 55+and can work a minimum of 15 hours a week, you can apply to be a Foster Grandparent volunteer with the Dept. of Human Services. There are certain health and other requirements.

As a Foster Grandparent volunteer, you’re a role model, a mentor, and a friend. Serving at educational institutions, you help set a child on the path toward a successful future.

CHILD AND FAMILY SERVICE

Volunteer Engagement Manager: Kevin Henry

808-342-2516 | khenry@cfs-hawaii.org

FOSTER GRANDPARENT PROGRAM

808-832-5169 | www.bit.ly/DHS_FosterGrandparent

Volunteering is a popular antidote to feelings of isolation that can occur as we age. Here are two programs that enable seniors to share their time and skills with younger generations.

According to Kathryn Coleman, Director at the Centers for Medicare and Medicaid (CMS), a final rule issued in April 2018 has redefined the “primarily health related” supplement benefit definition. As a result, CMS expects Medicare Advantage plan sponsors to begin offering services for enrollees needing assistance with Activities of Daily Living (ADL) or Instrumental Activities of Daily Living (IADL). Plans are not required to provide any of the services and restrictions may apply, but it is a first step toward utilization of Medicare insurance for long-term services. That’s great news for caregivers of Medicare beneficiaries on limited incomes who did not make provision for non-medical care as they age. The list below details possible options resulting from CMS’s new ruling. This list is not exhaustive.

Whether Medicare Advantage plans implement any of these services in 2019, or beyond, there will be a growing interest and high demand for long-term services and support as Medicare enrollees age.

MEDICARE MOMENT WITH MARTHA

A radio program with Martha Khlopin

KHNR-690AM: Sundays 9:30am–10am

808-230-3379 | getmartha@aol.com

According to Kathryn Coleman, Director at the Centers for Medicare and Medicaid (CMS), a final rule issued in April 2018 has redefined the “primarily health related” supplement benefit definition. As a result, CMS expects Medicare Advantage plan sponsors to begin offering services for enrollees needing assistance with Activities of Daily Living (ADL) or Instrumental Activities…

When a senior member of your family is in need of 24/7 care, it is fortunate that Hawai‘i has many professional, caring and dedicated homes and facilities to welcome them. What every family wants to know is: “Will my mom or dad be happy living in someone else’s home, eat right, and stay mentally and physically strong?” It may be even more important to you that your 80-, 90- or even 100-year-old family member lives in a facility that can assist them to improve their daily life.

Placing your loved one in a residential care home takes a lot of research. On your visit to the care facility, observe these few things:

Placing your loved one in a residential care home takes a lot of research. On your visit to the care facility, observe these few things:

Many facilities may have “respite” care to see how they would like living there. Let them make the decision for their happy, healthy and strong life.

AIEA HEIGHTS & WAIALAE SENIOR LIVING I & II

99-1657 Aiea Heights Drive | 2945 Kalei Road

808-488-5521 | 808-941-6940

www.aieaheightsseniorliving.com

When a senior member of your family is in need of 24/7 care, it is fortunate that Hawai‘i has many professional, caring and dedicated homes and facilities to welcome them. What every family wants to know is: “Will my mom or dad be happy living in someone else’s home, eat right, and stay mentally and…

People living with dementia (PLWD) have challenges with verbal communication: language comprehension, speech production, and vocabulary. But they are not unconscious to what is going on around them. Even as the brain declines, emotional intelligence is preserved. PLWD take in data visually rather than auditorily and react to what they think is happening. As caregivers we must remember that PLWD are really doing the best they can with the abilities they have left.

Try not to expect them to be the way they used to be. Accept them for who they are now and who they’re becoming. Promote independence by encouraging participation in meaningful activities. We all want to feel “of use” in this crazy world and PLWD are no different.

The feelings they may find hard to express are captured in this poem, inspired by a dementia patient.

MEMORY FRIENDS

Respite, Education & Consultation

Mapuana Taamu, Certified PAC Trainer

808-469-5330

mfriends808@gmail.com

People living with dementia (PLWD) have challenges with verbal communication: language comprehension, speech production, and vocabulary. But they are not unconscious to what is going on around them. Even as the brain declines, emotional intelligence is preserved. PLWD take in data visually rather than auditorily and react to what they think is happening. As caregivers…

Home healthcare providers are often asked what makes a better caregiver. The answer is that, while many factors come to mind, an interest in learning is high on the list, and essential to a caregiver’s progress.

Home healthcare providers are often asked what makes a better caregiver. The answer is that, while many factors come to mind, an interest in learning is high on the list, and essential to a caregiver’s progress.

For example, an important role caregivers have is recognizing when an individual’s health condition is changing. Those who can reflect and learn from these changes often develop into better caregivers.

Caregiving for a family member can be challenging enough. But whether this occurs suddenly or as a gradual decline in health, caregivers can learn more and better themselves starting with some basic tips:

In healthcare, caregivers are always learning, adjusting their knowledge and skills, and adapting to new information. This occurs even when a caregiver becomes the one being cared for, and experiences things from a new perspective. By continuing an interest in learning new things and being flexible, a caregiver can better themselves and the quality of life for others.

ATTENTION PLUS CARE HOME HEALTHCARE

Accredited by The Joint Commission

1580 Makaloa St., Ste. 1060, Honolulu HI 96814

808-739-2811 | www.attentionplus.com

AGING IN HAWAII EDUCATIONAL OUTREACH PROGRAM by Attention Plus Care — a program providing resources for seniors and their families, covering different aging topics each month. For caregiver training and upcoming topics, call 808-440-9356.

Home healthcare providers are often asked what makes a better caregiver. The answer is that, while many factors come to mind, an interest in learning is high on the list, and essential to a caregiver’s progress. For example, an important role caregivers have is recognizing when an individual’s health condition is changing. Those who can…