Siblingship describes the unique relationship between siblings. Siblings begin their relationship at a young age, and if they are fortunate, they reach old age together. They experience joys and setbacks, they laugh and cry — and they fight. Through the fighting, they can learn conflict resolution. Spouses join us in our adult lives. Friends often come and go. But no other relationship is quite like a siblingship.

When siblings fight as kids, it’s over property and fairness. Parents make sure property is divided up fairly — they are the ones to “divide up the pie,” so siblings don’t fight over things as much.

When parents die, siblings are called home to “divide up the pie,” this time, without parental supervision. In my experience, adult siblings fight over the same things that they fought over when they were kids: property and fairness. However, the parents are no longer there to referee and help divide up the pie fairly.

Estate planning can minimize the risk of fighting when parents die. If parents and the estate planning attorney don’t spend enough time anticipating and planning to minimize the risk of fighting, there exists a risk of fracturing, or worse, destroying this unique, wonderful relationship — the siblingship.

Siblingship describes the unique relationship between siblings. Siblings begin their relationship at a young age, and if they are fortunate, they reach old age together. They experience joys and setbacks, they laugh and cry — and they fight. Through the fighting, they can learn conflict resolution. Spouses join us in our adult lives. Friends often…

According to a recent study published by Ameriprise Financial, individuals in their 30s and 40s have received significant financial help from family and expect additional assistance in the future. And over a quarter of those surveyed said they received $25,000 or more.(1)

It’s admirable to see that parents want to go to such great lengths to help their children achieve financial success. Yet parents need to be mindful that they don’t inadvertently diminish their own success in doing so. As a financial advisor, here’s the advice I offer parents who want to give their adult children a financial head start without harming their own financial future: ■ Prioritize saving for your own retirement. It takes many years to accumulate the savings you need to retire comfortably. Your children are likely just starting their careers, while your time remaining in the workforce may be limited to five, 10 or 15 years. Putting yourself first isn’t a selfish move. It’s about being wise with your money. If you make it a priority to have enough saved when you retire, your kids won’t have to worry about providing you with financial support later in life. ■ Be strategic with your financial gifts. Like other monetary goals, it’s important to add gifts of cash to your overall financial plan. When you treat cash gifts separately, you shortchange other priorities such as retirement. What will it cost you to divert savings from your retirement plan? With a complete list of financial priorities, you can see how much you need to save to reach them all. ■ Consider alternate approaches to helping your kids. There may be ways to help your kids other than by dipping into savings. Encourage them to take financial responsibility when they can do so. Your college-bound son or daughter may be able to take out student loans at a low interest rate, which will reduce or eliminate the amount you need to contribute for tuition. Instead of writing a check to help your child buy a car or house, you might co-sign a loan to help them lock in a lower interest rate or more favorable repayment terms. ■ Have conversations about money. Your willingness to talk about your finances is a valuable example for your adult children. So, too, is your attention to your retirement savings. I encourage parents to invite their adult children to attend a financial planning session with a financial advisor. It’s a time to address money concerns and explore how actions today can affect your future finances.

According to a recent study published by Ameriprise Financial, individuals in their 30s and 40s have received significant financial help from family and expect additional assistance in the future. And over a quarter of those surveyed said they received $25,000 or more.(1) It’s admirable to see that parents want to go to such great lengths…

October through December brings an annual opportunity for seniors to review their health status and medical insurance plan to ensure coverage that suits them best.

All seniors 65 and over can have health insurance. If needed, no-cost government sponsored plans are a ready and available option. Hawai‘i seniors who have had changes in income, assets or disability status are encouraged to check eligibility and apply for coverage. Eligibility depends on many factors, including age, household size, assets and income.

For seniors with Medicare, Oct. 15 through Dec. 7 is known as the “Annual Enrollment Period.” During this time, people with Medicare can change their Medicare health plan and prescription drug coverage for the following year. To learn more about getting Medicare coverage and plan information, visit Medicare.gov or call 1-800-MEDICARE.

Regardless of coverage, don’t let the year go by without seeing your doctor. If you don’t have one, contact your health insurance plan to assist you or make an appointment with a clinic nearby. An annual checkup can be lifesaving. Community health centers will see patients for medical and/ or dental services regardless of the ability to pay. Learn more at hawaiipca.net.

October through December brings an annual opportunity for seniors to review their health status and medical insurance plan to ensure coverage that suits them best. All seniors 65 and over can have health insurance. If needed, no-cost government sponsored plans are a ready and available option. Hawai‘i seniors who have had changes in income, assets…

Seniors 65 years and older represent about a third of all pedestrian fatalities across the state. The Hawai‘i State Department of Transportation’s Walk Wise Hawaii program launched a partnership with First Insurance Company of Hawaii (FICOH) to stress the importance of visibility while walking — day or night.

Most pedestrian crashes occur between 6 pm and 6 am, when visibility is low. FICOH provided over 3,500 green reflective pedestrian snap-on wristbands and safety lights at senior outreach events across the state.

SOME SAFETY TIPS

Dress to be seen. During the day, wear brightly colored clothing. At night, wear reflective material on your shoes, hat or clothing.

Cross only at corners or marked crosswalks.

Always walk on the sidewalk. If there is no sidewalk, make sure you walk facing traffic.

Look left, right, left again and over your shoulder before you step into the street.

Keep looking and listening as you cross, until you reach the other side.

When crossing in front of stopped cars, make eye contact to be sure drivers see you before crossing in front of them.

If your organization would like to receive pedestrian safety wristbands, email Lance@tlcpr.com to book a pedestrian safety presentation. For more information, visit hidot.hawaii.gov/walk-wise-hawaii.

Seniors 65 years and older represent about a third of all pedestrian fatalities across the state. The Hawai‘i State Department of Transportation’s Walk Wise Hawaii program launched a partnership with First Insurance Company of Hawaii (FICOH) to stress the importance of visibility while walking — day or night. Most pedestrian crashes occur between 6 pm…

At its nine senior centers, the County of Kaua‘i Department of Parks & Recreation (DP&R) provides quality educational and recreational opportunities for growth and enhancement through an array of diverse programs and special events that promote community participation and environmental awareness while meeting the physical, mental, social and psychological needs of our island’s kūpuna.

■ Senior Classes & Activities: Kekaha, Waimea, Kaumakani, Hanapēpē, Kalāheo, Kōloa, Līhu‘e, Kapa‘a/Anahola (combined sites) and Kīlauea Neighborhood Centers serve as hubs for senior classes and activities, including hula, ‘ukulele, wellness, crafts, ballroom and line dancing, mahjong, Nordic Walk, yoga, meditation, chi gung, drumming, tai-chi, weightlifting and bingo. ■ Senior Pickleball: Pickleball continues to grow among the senior population, attracting well over 300 participants on Kaua‘i. Mini tournaments, leagues, classes and open play are offered at outdoor public venues and gyms across the island.■ Senior Mini Fun Day: In September, Kaua‘i DP&R holds competitive outdoor games, including Portuguese horseshoes, water balloon toss and bingo with prizes, entertainment and morning snacks. Seniors look forward to meeting up and mingling with friends from other senior centers. ■ Senior Craft Fair: The Līhu‘e Senior Center hosts a popular craft fair in October, offering a jumpstart on holiday shopping. Homemade wares, such as rugs, quilts, blankets and lei are sold. Bonsai plants are also on display, with knowledgeable seniors on-hand to share their expertise about cultivation and care. Strong community support has baked goods, pickled onions and other favorites selling out, so get there early. ■ Valentine Aloha Party: A well-deserved, popular “Mahalo Party” with a live band welcomes the members of all Kaua‘i Senior Centers in February. Kaua‘i firefighters serve as dance partners. Seniors enjoy a delicious buffet luncheon, with door prizes given away throughout the day, courtesy of Na Kupuna Council.

At its nine senior centers, the County of Kaua‘i Department of Parks & Recreation (DP&R) provides quality educational and recreational opportunities for growth and enhancement through an array of diverse programs and special events that promote community participation and environmental awareness while meeting the physical, mental, social and psychological needs of our island’s kūpuna. ■…

Help is available for veterans who have served our country and who now need assistance with caregiving — either as a caregiver or someone who needs care.

However, many veterans are not aware of the services available to them, a new AARP survey of veterans 45 and older reveals.

About half of those surveyed said they currently provide care for an adult loved one, relative or friend, or have done so in the past. But 60% did not know that the US Department of Veterans Affairs (VA) offers grants for home modification. The survey also found that nearly half (46%) need bathroom modifications in order to age in place themselves or to provide care for a loved one in their home.

That’s why AARP has two guides available for veterans and caregivers of veterans:

A new Veterans Home Modification Benefits Guide helps veterans navigate the VA’s $150 million program to help buy, build or modify a home to support long-term needs. Grants can help eligible veterans with up to $117,000 to pay for renovations, such as adding grab bars in bathrooms, installing ramps or widening doorways.

The AARP Military Caregiving Guide provides basic tips to help families through the caregiving journey and has tips and details of other VA caregiving programs.

Tips for military caregivers:

Talk about the medical and emotional needs of wounded warriors and caregivers of veterans.

Create a support system of family, friends and colleagues. You can’t be a caregiver by yourself.

Create a plan that enables you to respond to specific needs as they arise.

Seek professional support for information and resources from those with experience with military or veteran caregivers.

Care for yourself so you can sustain your energy and maintain your own health.

AARP HAWAI‘I (nonprofit) 1001 Bishop St., #625, Honolulu, HI 96813 808-545-6000 | hiaarp@aarp.org | aarp.org/hi AARP is a non-partisan organization dedicated to empowering Americans 50 and older to choose how they live as they age.

Help is available for veterans who have served our country and who now need assistance with caregiving — either as a caregiver or someone who needs care. However, many veterans are not aware of the services available to them, a new AARP survey of veterans 45 and older reveals. About half of those surveyed said…

Physical health enables us to lead active lives, with food intake being a primary determinant. The food we consume not only provides us with energy, but also influences our weight, diversity of gut bacteria, immune system strength, inflammation levels and rate of aging.

The nutrient density of our produce is an important factor. Studies reveal that most vegetables can lose up to 55% of their Vitamin C within a week, and spinach can lose 90% within just 24 hours. This underscores the importance of growing your own produce or purchasing fresh fruits and vegetables from local farmers.

Fruits and vegetables are rich sources of anti-inflammatory antioxidants, sugar and fiber, benefiting both us and our gut bacteria. Since 80% of our immune system resides in the small intestine, maintaining good gut health is crucial. Poor gut health can lead to inflammation and autoimmune disease.

Nutrient-dense foods

High fiber: legumes (beans), leafy greens and vegetables.

Anti-inflammatory: turmeric and ginger.

Antioxidants: fruits and berries.

Keep in mind that the foundation of good physical health relies heavily on nutrient-dense foods for ourselves and our gut bacteria.

Physical health enables us to lead active lives, with food intake being a primary determinant. The food we consume not only provides us with energy, but also influences our weight, diversity of gut bacteria, immune system strength, inflammation levels and rate of aging. The nutrient density of our produce is an important factor. Studies reveal…

Practicing yoga can improve quality of life for seniors. As with any exercise regimen, check with your doctor before beginning yoga for the first time as a senior citizen.

■ Reduce stress: With its combination of low-impact exercises and breathing techniques, yoga can have a relaxing effect on the body and mind, leading to a sense of improved overall wellness. Some forms of yoga have also been shown to have positive effects on brain health, which may help combat the cognitive decline often experienced by seniors. ■ Improve mood: Through stretching, breathing, movement and meditation, there is evidence that yoga has mood-enhancing properties because it can inhibit both physiological stress and inflammation that can adversely affect behavioral health. ■ Improve posture: – Improve core strength. When the core muscles of the body are strong, the spine is supported to maintain proper alignment. – Improve bone density. The weight-bearing aspects of yoga may slow the decrease in bone density that leads to osteoporosis. – Greater awareness of the body. Through yoga’s focus on the body and breath, seniors can feel more in control of their bodies, which makes them more likely to stand tall with confidence. ■ Improve sleep: Older adults are more susceptible to sleep disorders like insomnia. Studies have shown that yoga improves sleep quality after just six months of practice. ■ Increase flexibility: Yoga promotes flexibility through gentle stretching, breathwork and increased internal awareness. ■ Reduce risk of falls: Yoga can prevent/reduce falls by strengthening muscles, improve balance, calm the mind and bring focus into the body. ■ Improve mobility: Stiff muscles and joints are common among senior citizens, but practicing yoga can gently support your range of motion. ■ Increase strength: Even the most gentle yoga can strengthen your body. Using a combination of gravity and your own body weight, yoga can help build lean muscle to make you stronger. ■ Increase social interactions: People may find themselves increasingly isolated as they get older. Attending group yoga classes is a great way to stay engaged within your community. ■ Encourage mindfulness: Yoga focuses on breathing and listening to your body. Looking inward in this way helps create a deeper connection between your mind and body.

Practicing yoga can improve quality of life for seniors. As with any exercise regimen, check with your doctor before beginning yoga for the first time as a senior citizen. ■ Reduce stress: With its combination of low-impact exercises and breathing techniques, yoga can have a relaxing effect on the body and mind, leading to a…

Real estate is often considered one’s residential or rental property. But as we age, real estate can become a burden. If this is you, you’re not alone.

Meet “Mrs. Lee,” a longtime homeowner who finds her home is too big and too much work to maintain. She receives support from a real estate planner who helps her understand her options and she learns ways to transition to a more stress-free lifestyle.

“Mrs. Wong,” is concerned about capital gains taxes and her kids fighting over inheritance. She’s been told that 70% of families will fight after their parents pass away. So she removes the burden of the rentals by selling them and creates a plan to eliminate capital gains taxes with a 1031 exchange. She is ecstatic that she can remove the potential family disputes.

“Mr. Smith” is tired of the worry of his rentals and dreams of a stress-free retirement. Collaborating with his real estate planner, he sells his rental via a 1031 exchange and replaces it with a Delaware Statutory Trust (DST), achieving financial freedom, reducing property management hassles and avoiding capital gains taxes.

The moral of these tales: With the right guidance, a real estate plan can help seniors achieve financial security and peace of mind.

Real estate is often considered one’s residential or rental property. But as we age, real estate can become a burden. If this is you, you’re not alone. Meet “Mrs. Lee,” a longtime homeowner who finds her home is too big and too much work to maintain. She receives support from a real estate planner who…

Paying too much but don’t know how to get a better price? Haggling might help. Negotiating prices via haggling can save savvy shoppers money, especially on big-ticket items like homes, vehicles or expensive services. Although it can be intimidating, haggling is common. When done respectfully, it can create a healthy marketplace. Here are a few tips to help:

Tips for New Hagglers

Research First: Find what a fair market price is and use BBB’s Get-a-Quote tool (bbb.org/get-a-quote) to get multiple quotes, empowering you to negotiate reasonably and knowledgeably.

It’s a Conversation: Think of haggling as a conversation communicating your needs and expectations to get the best value for your money.

Be Willing to Walk Away: If the seller doesn’t meet your expectations, be prepared to go elsewhere. Showing you aren’t desperate increases leverage.

Be Respectful: Always maintain a polite attitude, striving for a satisfying middle ground for both parties. When done right, haggling can be enjoyable, help you identify the right company to purchase from and save you thousands of dollars on your next big purchase.

Paying too much but don’t know how to get a better price? Haggling might help. Negotiating prices via haggling can save savvy shoppers money, especially on big-ticket items like homes, vehicles or expensive services. Although it can be intimidating, haggling is common. When done respectfully, it can create a healthy marketplace. Here are a few…

This refreshing salad is so easy to make, especially when I bake the bacon in the oven.

I usually double or triple the salad dressing recipe so there is plenty on hand for everyone to enjoy.

While I can’t remember how I got this recipe, my family has enjoyed this salad for over 40 years. When I first “served” this salad at our “tennis gang” potluck dinner, it instantly became their favorite.

Our tennis friends have been together for over 40 years now. Even though some of us no longer play tennis, we all get together because we enjoy each other’s company. It still always makes me smile when someone brings this salad.

Salad Ingredients: 1 lb. spinach 2 hardboiled eggs 2 tomatoes 5 bacon slices (425 degrees, 10 minutes) 1 can Chinese noodles 2 can water chestnuts, sliced 1 can mandarin oranges (Optional add-ons: mushrooms, chopped apple, avocado, bean sprouts, any of your favorites!)

Dressing: 3/4 cup white sugar 1 cup salad oil 1/2 cup apple cider or Japanese vinegar 1/3 cup ketchup 2 Tbsp. Worcestershire sauce 1 tsp. salt

Directions:

Wash, dry and tear spinach leaves.

Cut hardboiled eggs into quarters.

Slice tomatoes into bite-sized wedges.

Break bacon into crumbles.

Combine all salad ingredients in wooden bowl.

For the dressing, mix the sugar, salad oil, vinegar, ketchup, Worcestershire and salt in a small bowl. Blend well.

Pour desired amount over salad ingredients. Toss lightly and serve immediately.

Prep time: 30 minutes | Serves: 6

Do you have a favorite recipe and story to share? For consideration in the next issue, include a photo and mail them to Generations Recipe, PO Box 4213, Honolulu, HI 96812, or email them to Cynthia@generations808.com.

This refreshing salad is so easy to make, especially when I bake the bacon in the oven. I usually double or triple the salad dressing recipe so there is plenty on hand for everyone to enjoy. While I can’t remember how I got this recipe, my family has enjoyed this salad for over 40 years.…

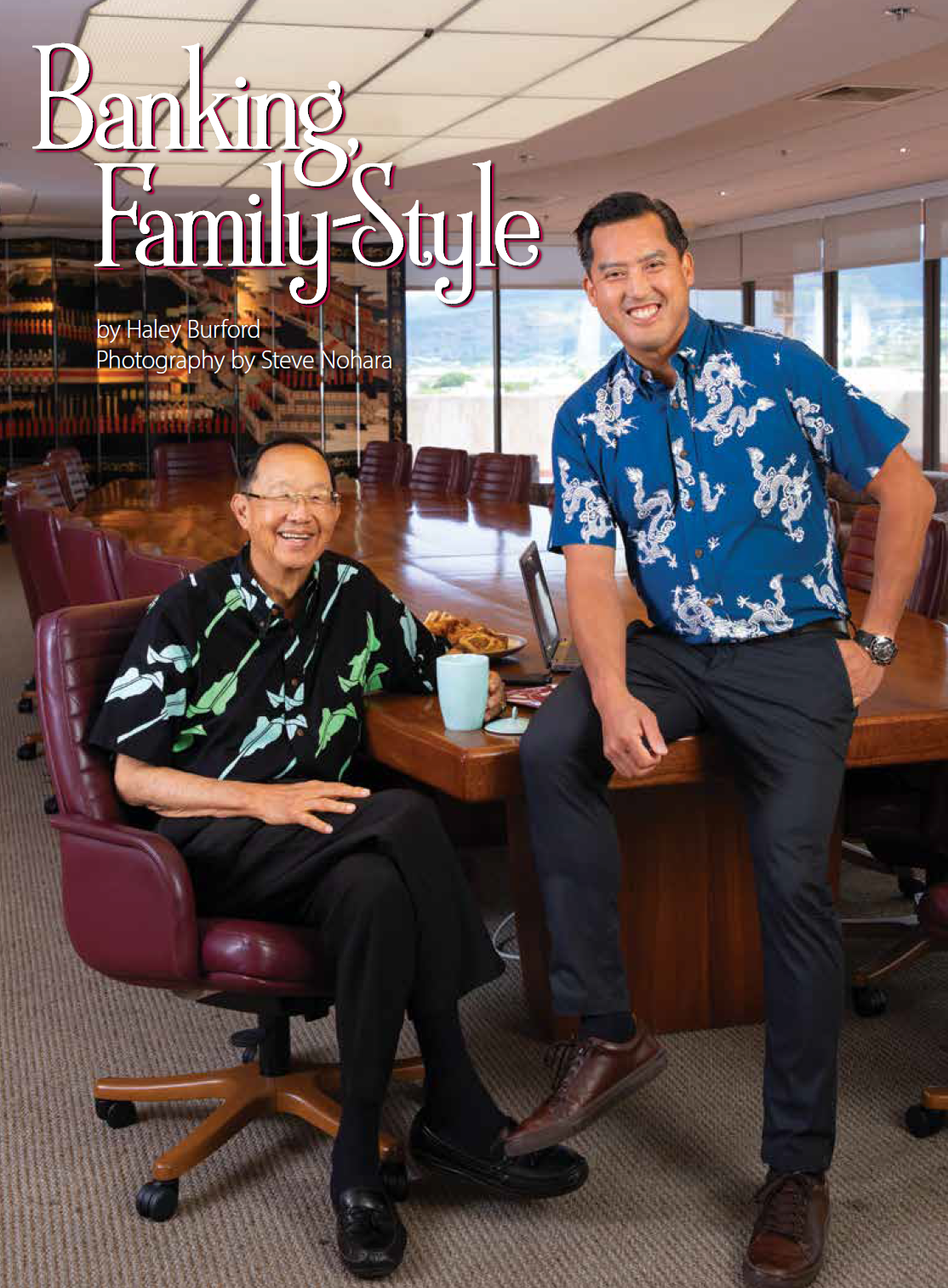

Story by Haley Burford Photography by Steve Nohara

The words “family” and “business” are not mutually exclusive to Hawaii National Bank’s owners and operators. HNB is at once a “business family” and a “family business.” For the last 64 years, the Luke family has supported small businesses, family businesses and each other with their intrinsic knowledge and practical experience. They know what it takes to run a family business because they are a family business. But a name plaque on a desk at the bank is not assured simply for being a family member alone. A member of the Luke family must earn that honor by having the aptitude, talent and passion for the banking business.

The Luke family’s community bank has thrived, as have their clients, utilizing a business model that assesses intangibles, prioritizes Hawai‘i’s people and incorporates integrity, philanthropy and responsibility as its core values.

The family’s principles, policies and values govern the way the bank engages in business, establishing a code of conduct that drives employee behavior at all levels and builds trust between the bank and its customers. These foundational family standards guide the company’s actions, influence its culture and determine how the bank interacts with customers, employees and the community. They serve as a compass for decision-making and help align the goals and vision of the company with the behaviors of its workforce.

Big bang beginnings

Hawaii National Bank (HNB) celebrated its grand opening with a bang and the pop of 10,000 firecrackers in Honolulu’s Chinatown on Sept. 19, By the end of that very first day, the bank had received about $6.25 million in deposits, setting a national record for first-day bank deposits in the United States. From that point onward, HNB has maintained its status as a top-tier financial institution in Hawai‘i.

Hawaii National Bank prides itself on being locally owned and operated. It is through their highly personalized and intimate philosophy that HNB has garnered and retains a clientele that consists of not only individual account holders, but families and small businesses, too. Brought into being by KJ Luke and a group of local businessmen in 1960 as a publicly owned bank, upheld by Warren Luke and now headed by the third generation, Bryan Luke, HNB and its nine branches continue to grow with our ever-evolving Hawai‘i, maintaining its well-deserved reputation every step of the way. HNB is a community bank, with all decisions made locally, and they are traditional in the sense that both commercial and retail banking services are provided to customers. HNB aims to lead us down the path of financial literacy, security and relationship-building they feel we all deserve.

An upward trajectory

KJ Luke began his work life at his father’s general store on the Big Island. Years later, he graduated from the University of Hawai‘i with a degree in accounting. While applying for a job at a local bank, he ran into his accounting professor, who encouraged him to pursue an advanced degree instead of a job. Luke responded by saying, “I will send in an application, but if I don’t get accepted, I want you to help me get this job.” Luke was accepted to Harvard Business School, earning an MBA (Master of Business Administration). He was later awarded the school’s highest honor, the Alumni Achievement Award, becoming the very first Chinese-American to earn such an accolade.

KJ Luke went on to become one of Hawai‘i’s most successful businessmen and real estate investors. Among his many achievements in the realm of his business ventures was his idea of building a new bank to make the most of Hawai‘i’s booming economy at the time. He wanted to prioritize building strong interpersonal relationships and taking care of Hawai‘i’s diverse local population.

Taking on the responsibilities of president and chairman of this new project, Luke applied and then was approved for a federal charter to open the only national bank in Hawai‘i.

Thus, HNB came into being, and was (and still is) highly regarded among the state’s people. Priding itself on being the “Home of Warm-Hearted Bankers,” through three generations of leadership, Hawaii National Bank strives to be there for the people, throughout all stages of their lives.

A legacy of excellence

After KJ Luke came his son, Warren. Warren Luke is the current chairman of HNB. Like his father, Warren attended Harvard Business School after obtaining his undergraduate degree at Babson College in Massachusetts. Championing the value of education for Hawai‘i’s (and the world’s) youth, Warren also involves himself in various nonprofits and boards, including Harvard Business School’s Asia Pacific Advisory Board and through supporting the Harvard Center Shanghai.

The third generation of Luke family legacy of excellence is Warren’s son, Bryan, the current president and CEO of HNB. Like his father and his father before him, Bryan also attended Harvard Business School and advocates for strengthening Hawai‘i’s economy, environment, education and entrepreneurship. He serves on multiple local and national boards, including Hawaii Community Reinvestment Corporation, the Pacific and Asian Affairs Council and the Rehabilitation Hospital of the Pacific.

The achievements of these men are not few. Their desire for change and capacity for compassion are not small.

Of course, all of these accolades and accomplishments are impressive, but to the Luke family, what they really celebrate are the close relationships they have built and kept with their clientele, and the family businesses and individuals they have worked with.

The family business

One of the core messages that Hawaii National Bank wants the people and small/family businesses of Hawai‘i to be aware of and understand is that they know what it takes to run a family business — because they are a family business.

Bryan spent time in the Bay Area and shared how he disliked being removed from a hands-on work environment. “I’d value businesses and intangible assets,” says Bryan. “I’d consider a lot of things you can’t see, touch or feel.”

After returning to Hawai‘i and working at the bank, Bryan realized he was right where he belonged. “Coming back home and working with local families and really seeing what we do and how we help our customers and businesses — and therefore, their families and the overall community — just made things way more tangible.”

Bryan feels that working at HNB is much more rewarding because the help provided to their customers can actually be seen making a palpable difference in their lives.

Warren interjects some insight regarding the evolving nature of banking and services today: “Banking is changing now because of IT [information technology] systems and what’s available online. So we have a lot of younger customers say, ‘Why do I need a banking relationship?’”

“There will be some time in your life when you’re going to need a relationship for a loan or understanding what you want to do — if you want to acquire a business or buy a house, you will need to go in and talk to a banking officer, or relationship officer,” says Bryan.

“That’s what we really concentrate on: relationships.” Bryan adds that HNB may be compared to the private banking group of a larger bank, as they offer more personalized service and opportunities to build a relationship with your banker.

Consistency, constancy & continuing change

When Warren began at the bank, he assessed the situation and realized that many of HNB’s senior officers were on the verge of retirement. He looked to the board about hiring a consultant. Bryan had worked for a consulting company, so the board hired him to do a project during the summer. He proved himself. They liked what he did, and the bank hired him.

“All of a sudden, I replaced my senior officers with officers in their 30s — it was a big change,” says Warren. With this change came the need to also update their IT systems, and it was a work-in-progress then just like it is today, especially with the rise of AI (artificial intelligence). He jokes, “So, working with the young people is fine.”

HNB has undoubtedly undergone changes in the 64 years it has been in existence. Bryan’s challenge was keeping the good parts of what the bank excels at but also evolving for the future.

“When I came onboard 18 or 19 years ago, we were about a $300-million bank in asset size,” says Bryan. “We’re at about $800 million now. One of the things we did really well when I first started was the relationship — the close contact that we had with a lot of our longtime customers. We were going through a generational transition and a lot of our customers were, as well, so the question became, how do we adapt for the next generation of leaders?”

To Bryan, figuring out how to maintain that close contact HNB prioritizes was paramount. “The fear that you have is twofold: one, not being able to keep up in terms of technology, but, two, maintaining that personal touch you have with your customers,” says Bryan. “You have to use a combination of both things and we spend a lot of time working on that.”

The business of family

The other thing Warren feels strongly about is upholding family. “I’ve been lucky because I’ve worked a lot in education. I was in a group to help with input on the family business practice at Harvard Business School. Now, there are a lot of schools that have family business sections that concentrate on family businesses. At Harvard, we concentrate more on the business family, because you have to work with a family to keep it together to make sure that the business can survive. If the family stays together, the business can survive a lot of different things. If the family doesn’t stay together, it’s very difficult.”

Why do Warren and Bryan feel so strongly about finding a balance between being a family and being a business? When asked to what extent it is important for HNB to be family-owned and operated with regard to their clientele, Warren answers, “We really wanted to take care of local businesses. Helping local business is our business.” Many local businesses in Hawai‘i are family-owned and locally owned, so HNB feels a duty to take care of them. “We wanted to be a community bank — a smaller bank. We have a lot of big banks in town and they cater to the bigger businesses, many of which are owned by companies headquartered on the mainland. As a community bank, in the long run, if you want to build your banking practice, I felt that it was easier to operate as a family-owned or private company than a public one. We started as a public company, but when you go through tough times in the economic sense, we had to ensure that we kept some of the equity to handle our growth and yet still take care of the local ownership, so that’s why the decision was made to go private.”

“Like my dad said, our market is locally owned, closely held companies, and because we are also one, we are better able to relate to our customers.”

The Luke family and HNB look at the “business family” as opposed to the “family business.” “When the next generation comes in and wants to make changes, the older generation doesn’t agree,” says Warren. “The business climate changes; what’s happening in town changes. You have to go with the flow and do it properly.”

Spanning the generation gap

The generational road of HNB’s leadership, transitioning from father to son, older to younger, is not without bumps along the way. When asked about the sorts of challenges that can come up when operating a generational, locally owned family business, Warren says, “It’s kind of separate. When you have a family-owned business, you must still look at the qualifications of the people running the business. The question is always, what’s more important: running the business like you run a family, or running it like a corporation? We have to do both. We must have qualified people coming in, so we have to make sure that the family members are qualified.”

“The other thing is generations change and their outlooks change.” Warren adds. “So, when it’s time for older generations to step aside and turn over the business to the younger, you must first make sure they’re qualified, then, you have to let them work with your current customers, because customers think differently now and expect different things.” With a laugh, he finally says, “Sometimes, the older generation has to learn to bite their tongue. Let the younger ones make mistakes, ‘cause they learn from their mistakes.”

Bryan finds it interesting how generational change will often bring with it a completely different way of thinking and operating a business: “I think we were pretty careful in that we want to make sure we keep the core of who we are, and then supplement it with — whether it’s new technology or whatnot — changing the company to move it into the future.” Bryan likes to say that half of his job is moving the company forward and the other half is not messing things up. “I think the benefit of that, too, is the fact that I am the third generation at the bank. When my dad came in and worked for his father, I got to see all the good and bad things, so it was a little bit easier for me to come in, since he already experienced that once before.”

When Bryan first started at the bank, he was often asked how parents can get their kids to come back and work for them — “the way you work for your dad?” He pondered these questions, assessing the benefits and drawbacks one should consider regarding staying at a mainland job or coming back home to work — a decision he had to make, and feels he made correctly.

The currency of philanthropy

HNB and the Luke family work with various nonprofits in the spirit of charity.

Bryan says, “I think a lot of that stems originally from my grandfather and a lot of what he did. My dad also does a ton of things — locally and internationally.” Warren has served on the local and national boards of the Red Cross and the United Way of America, as a trustee of Punahou Schools and Babson College, the Federal Reserve Board of San Francisco, the Pacific Basin Economic Council headquartered in Hong Kong, and is currently on the Asia Pacific Advisory Board for Harvard Business School. He is chairman of the Pacific and Asian Affairs Council, where Bryan is currently a board member. Bryan is on the board of Hawaii Community Reinvestment Corporation, among other organizations.

His auntie Loretta Yajima founded the Children’s Discovery Center in 1989, and his auntie Janice Loo is president of the Takitani Foundation and a director of Rehab Hospital of the Pacific.

“Really, it’s about starting from an early age through your whole life.” Warren found by serving on the boards, many problems and topics are similar. Bryan connects this philosophy to the life cycle of a bank customer. The life cycles of people involved in the community carry over, crossing boundaries and overcoming challenges to cultivate a more learned, cohesive Hawai‘i.

A future you can bank on

As for plans for the future of HNB, Bryan and Warren outline some things that have changed and will change, but also things that will remain the same. “At the heart of the whole thing is that we are a community bank, and we intend to remain a community bank.”

Bryan feels that it is their duty to be a part of this community in Hawai‘i and remaining so. “It’s not just about growth, it’s about helping build the local community.”

As a person in a unique position — learning from his father and now teaching his son, Warren has seen both sides as the bank has grown. “I just think that for Hawai‘i, locally owned businesses and family businesses are instrumental in helping the development of the economy and making sure the local people get taken care of.”

While times change, HNB’s integrity, philanthropy, responsibility and advocacy for Hawai‘i’s people and businesses won’t. Warren and Bryan Luke continue working to fulfill their mission of helping their customers achieve their goals.

Figuring out what is best for the people of Hawai‘i remains their priority — the “numbers” are just one side of that. For almost 65 years, Hawaii National Bank has been whole-heartedly here for the people — and so will it be for generations to come. You can bank on it.

The words “family” and “business” are not mutually exclusive to Hawaii National Bank’s owners and operators. HNB is at once a “business family” and a “family business.” For the last 64 years, the Luke family has supported small businesses, family businesses and each other with their intrinsic knowledge and practical experience. They know what it…