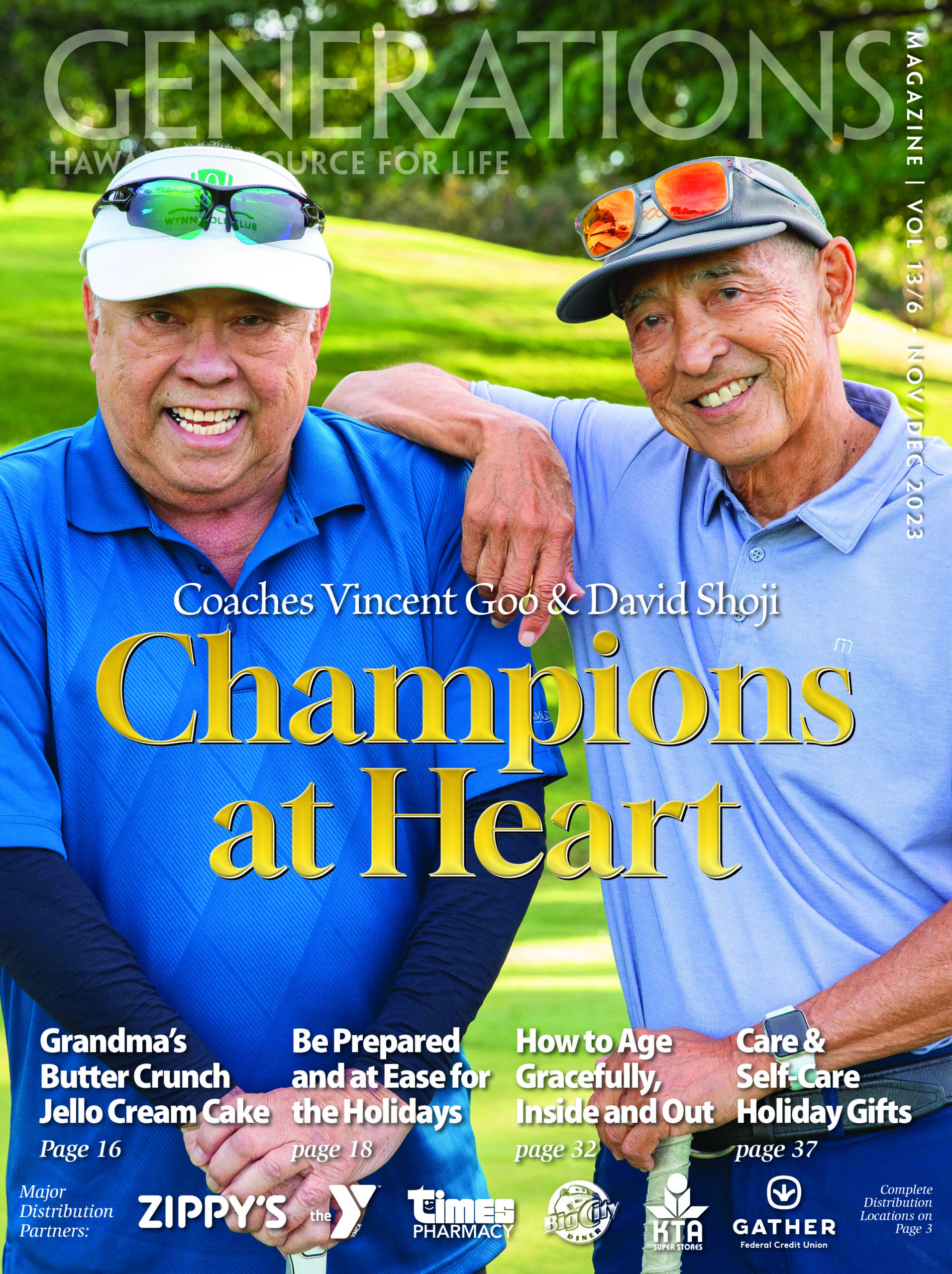

Chances are that you’ve heard of Dave Shoji and Vince Goo, two of Hawai‘i’s most beloved coaches. Known far and wide for their stellar coaching careers at the University of Hawai‘i at Mānoa (UHM), these individuals boast hundreds of wins and have earned the titles of the winningest coaches for their respective programs — for Shoji, volleyball, and for Goo, basketball. Today, the coaches stay active in their respective sports, along with playing rounds of golf, surfing and advocating for Hawai‘i’s kūpuna through their work with Hawaii SHIP (State Health Insurance Assistance Program).

Chances are that you’ve heard of Dave Shoji and Vince Goo, two of Hawai‘i’s most beloved coaches. Known far and wide for their stellar coaching careers at the University of Hawai‘i at Mānoa (UHM), these individuals boast hundreds of wins and have earned the titles of the winningest coaches for their respective programs — for Shoji, volleyball, and for Goo, basketball. Today, the coaches stay active in their respective sports, along with playing rounds of golf, surfing and advocating for Hawai‘i’s kūpuna through their work with Hawaii SHIP (State Health Insurance Assistance Program).

For Coach Goo, the most vivid memories of his coaching career — “my most happiest times” — are not the victories or the championship wins. He and his assistant coaches put a lot of work into the academics for their players, encouraging them to graduate. In terms of their grade point average (GPA), the Rainbow Wahine women’s basketball program was the top team out of all the UH sports for a number of years. Although Vince Goo is no longer on the court, his dedication to community and to guiding, not only the youth but all those around him, still shines through in what he does today.

Coach Shoji retired in 2017, after a 42-year career that included both highs and lows. From the time he first became their coach, Dave Shoji has been avidly supportive of the Rainbow Wahine women’s volleyball team and is a strong advocate for other women’s athletics programs. He was the first fulltime coach of any women’s program at UH, and his hard work helped “put them on the map.” Dave still dedicates himself wholly to guiding and helping others, most recently through his community service and encouragement of healthy living for kūpuna. He puts his all into everything he’s involved with, rooting for everyone around him.

VINCENT GOO

VINCENT GOO

Known by many here as simply “Coach Goo,” Vincent Goo had a 20-year coaching career with UH Mānoa’s Rainbow Wahine basketball team, during which he earned the title of winningest coach in the program’s history. Coach Goo retired in 2004, but continues to care for and mentor the people of Hawai‘i through his dedication to the community in various acts of service.

Born on O‘ahu in 1947, Vince was raised here and attended Kalani High, moving on to Southern Oregon State University (SOSU), where he received his degree in physical education in pursuit of becoming a PE teacher. “That was my best class. And the easiest class!” After graduating from SOSU with a bachelor’s in physical ed, Vince came back to Hawai‘i to teach at Castle High School in 1969, and he would continue on at Castle for seven years before teaching at Kaiser High School for another eight.

Vince’s introduction to a legendary coaching career seemed small: He started as a part-time assistant at UHM, where he met Bill Nepfel, another well-known figure in Hawai‘i sports, who was the women’s basketball coach at the time. The two quickly became friends, regularly playing pick-up ball together and hanging out. Several weeks later, Vince got the call.

“You’re gonna like it!”

“So, he calls me out of the blue one day and he goes, ‘Hey, I want you to be my assistant coach.’ I said, ‘Bill, what are you doing?’ That year, they went to the Final Four. I’d never seen the UH women’s team play — I was just coaching boys’ basketball. He said, ‘Oh, you’re gonna like it, you’re gonna like it! Come up to the gym, Gym 2, we play pick-up every day.’ So, I went up there and I was really impressed — they were shooting jump shots from free throws. Bill only had one position aside from himself, and that was part-time assistant coach and he would have to get someone who had a full-time job. I was still teaching at Kaiser, so when he offered me the position, I said, ‘Ah, OK, I’ll give it a try.’ I jumped in with him and I was there for three years. I was lucky I got the job here, at the University of Hawai‘i. Everything kind of fell into place.”

Coach Goo became the winningest coach in program history, boasting a 334–116 win rate. He was assistant coach for three years and head coach for 17, totaling a 20-year career with the Rainbow Wahine. For Goo, however, it was always more than just basketball. The renowned coach had three rules his players had to follow, and they’re as simple as ABC: Academics, Basketball, and citizenship. Putting academics first was no coincidence. Coach Goo has pride in knowing that all but one of his players were able to graduate with their degree.

Wins on and off the court

Wins on and off the court

“I thought, when I took over at UH, ‘How can we be the best in something? We’re not gonna win every game, we’re not gonna make every free throw. We’re gonna lose games, we’re gonna miss free

throws. But what if we graduate everybody?’ So, that’s what we set out to do. We ended up being the top GPA team out of all the sports for a number of years. I think we set the bar for all the other teams. All our athletes maintained a 3.0 or better, so that was a pretty good accomplishment.”

Goo’s most memorable moments in his career as Rainbow Wahine basketball coach have little to do with the games themselves. They relate to something as simple as his ABC rules: Commencement Day. Specifically, presenting lei to the graduating student-athletes. “We had a tradition that, when a player graduated, we would take their photograph — their mugshot, just in their jersey — and put it up on my office wall. It was only when they graduated that they’d come and put their picture up there. It never had anything but their jersey number, the years that they played, and their major. It never had anything else about basketball, about how many points, or how many rebounds, or whatever.”

Coach Goo retired in 2004, but even today, he still involves himself with sports via a community-driven approach. “Well, I don’t go to a lot of the games, but I support the teams and I’ll call a coach and give some words of encouragement. I try to keep up with the sports and, obviously, women’s basketball. I’ll give them a shout on the voicemail after games — if they played well.” With a laugh, he adds, “If they didn’t, I try not to say it on TV.” Though he doesn’t attend all sports games, he never misses a Rainbow Wahine basketball game. Goo co-hosts game-time interviews and analyses with UHM radio and TV play-by-play announcer Scott Robbs and Nani Cockett, who played for Coach Goo at UHM. At one of the games he announced for, Scott asked Vince how many kids he had. “I said, ‘Four.’ And Nani says, ‘Oh, don’t worry. Coach didn’t raise them. Mrs. Goo did. He was too busy trying to raise us.’”

It’s obvious that Goo enjoys so many aspects of this activity — from the co-hosting, the immersion, and, overall, the fun. Goo carries his passion for basketball and teaching with him today.

Work and play in retirement

Aside from still being engaged with the sports scene, Vince cherishes newfound hobbies and passions coming up in his retirement. His hobbies include: “Sweeping and mopping the house. But don’t talk to my wife, ’cause she’ll deny that! I play a lot of golf. And people are always asking me, ‘Hey, how’s retirement?’ I tell them it gets better every week. ‘Don’t you lose track of the days?’ No, you just wake up in the morning, go get your paper on the driveway — if the paper is thick, you know it’s Sunday.” And “Coach Goo” continues to advise and educate his community. He is especially proud of the work he and “Coach Shoji” participate in with Hawaii SHIP.

“With Dave and Jim Leahey, we did three commercials together. Since Jim passed, Dave and I have done two commercials. SHIP is a volunteer group and they’re wonderful, really wonderful. One day, I guess the commercial was on, and my grandson comes running downstairs, going, ‘Hawaii SHIP today!’ I happened to be sitting there, thinking, ‘What am I gonna do about this bill I got?’ Wait a minute! Maybe I should call them. I called them the next day and they called back 20 minutes later with information. That was terrific! I’ve called them a few times since. If you call Medicare, you’ll get all the prompts, you know, call this number, press 1, press 2, press 3, and even then, your category never comes up, right? So, who do you talk to? It’s tough.”

As for why he and his friends chose to work with Hawaii SHIP, Vince says, “They called us. They thought, ‘Hey, let’s get these old fuddy duddies, all three guys are retired.’ We might have a good connection with older people. From what I hear, we hit it off pretty good.”

Coach Goo recalls with fondness his friends, family, and the players he devoted many years of his life to. While proud of his achievements, he takes every opportunity to give credit to the community that took care of him and that he cares for. This legacy of care and mentorship, that he continues to hone, is something everyone can aspire to, no matter their age.

Shoji on Goo: We grew up fairly close to each other and were friends in grade school. So, we go way back. We went separate ways for a while, but then reunited at UH: two local boys who grew up in the sports world, ended up coaching at a major college in major sports. I really respected Vince as a coach, and we both were proud of where we came from and how we got the programs to be respectable.

David Shoji

David Shoji

Coach David Shoji is the now-retired coach of the UH Rainbow Wahine volleyball team. His incredible star-studded career spanned 42 years wherein he earned the title of the winningest coach in the program’s history. Today, Dave can be found playing some rounds on the golf course, catching waves and serving his community in several ways.

Dave Shoji was born in California in 1946, moving to Hawai‘i at the age of three, where his father, Kobe Shoji became a well-known expert in sugar cane production. Though he was born in the Golden State, Shoji’s upbringing was embedded in aloha. He attended public school here until the ninth grade, then the family moved back to Southern California when his father had to go overseas for work. Dave graduated from Upland High School, balancing academics with participation in three sports — baseball, football, and basketball.

The University of California at Santa Barbara (UCSB) is where the legendary coach first learned how to play volleyball. A naturally gifted athlete, Shoji earned All-American honors as a volleyball player in 1968 and ’69 while completing a degree in physical education. After graduation, he joined the army, serving for two years before returning to Hawai‘i to further his education at UHM in hopes of becoming a physical education instructor.

He had no clue that this decision would change his — and countless others’ — life forever: “I was just trying to be a teacher. I was hired to coach the UH women’s volleyball team — it was a parttime job. It wasn’t really something I intended to do for a long time. It was just kind of a job to keep me financially going and then it turned out to be, after a few years, a full-time job. I happened to stay for 42 years!”

From the ground up

Coach Shoji would go on to cultivate an iconic program in Hawai‘i sports and a legendary coaching career: over 1,000 wins, multiple national titles, 22 combined awards of conference and region Coach of the Year and much more. He has been named to the list of All-Time Great Coaches by USA Volleyball and the Hawaii Sports Hall of Fame. Like Goo, it was always more than just the wins for Coach Shoji. “Back when we started coaching, women’s athletics were just an afterthought for the University of Hawai‘i. It wasn’t like it is today; it was pretty spartan. We didn’t have much, but we love the sport. Both Vince and I love to coach and love the sport, so that’s why we did it — out of love for the sport.”

He looks back on these memories fondly. The most fulfilling part of coaching and mentoring his players for so many years is recounted with as much reverence and passion today as he felt when the events occurred. “There are so many highlights, it’s hard to pick one. But I think the first big event was winning the national championship in 1979, where we had been close — we’d been runner up and third place up until then — and in 1979, we finally won the national championship.” That win “kind of put us on the map, so to speak, and people here in the state started to identify with us. We would fill Klum Gym back in the day and they started to televise our matches which made us even more popular. So, that part was exciting — to be on the ground floor, on television, and people were actually coming to see us play. When the arena opened in 1994, we started attracting real big crowds of eight to ten thousand. Our program turned out to be a money-making sport for UH, which was pretty rare in college athletics — that a women’s program would actually make money for their school. That was exciting to be around.”

He looks back on these memories fondly. The most fulfilling part of coaching and mentoring his players for so many years is recounted with as much reverence and passion today as he felt when the events occurred. “There are so many highlights, it’s hard to pick one. But I think the first big event was winning the national championship in 1979, where we had been close — we’d been runner up and third place up until then — and in 1979, we finally won the national championship.” That win “kind of put us on the map, so to speak, and people here in the state started to identify with us. We would fill Klum Gym back in the day and they started to televise our matches which made us even more popular. So, that part was exciting — to be on the ground floor, on television, and people were actually coming to see us play. When the arena opened in 1994, we started attracting real big crowds of eight to ten thousand. Our program turned out to be a money-making sport for UH, which was pretty rare in college athletics — that a women’s program would actually make money for their school. That was exciting to be around.”

Preserving family, health, and community

David Shoji’s reputation precedes him. When people hear his name, few wouldn’t recognize the legendary Rainbow Wahine volleyball coach. Though Dave is no longer on the court, his life now is still just as colorful and busy. He manages to stay active not only in terms of his physical health and community, but he also is very much engaged in his family life.

“My wife and I, we both love sports. Our two boys played volleyball in high school here locally and went on to play collegiately at Stanford. They won a national championship at Stanford, which was really exciting for everybody. They went on to play professionally, and both sons made the 2016 and 2020 Olympic teams for the USA. Kawika, the older one, has just retired from professional volleyball and Erik, the younger son, is still playing. Our daughter, Cobey, married a football coach — he coaches at Alabama — so a lot of our life now is just following their teams. We’re also into being grandfather and grandmother! We have four and one on the way.”

Dave enjoys the relaxed pace of retirement, but he’s far from idle. “I’ve always golfed, so that’s still in the picture, but I took up surfing later in life. I’m probably surfing two or three times a week. The other things that old guys do are, you know, we garden, we cook, we babysit the grandkids. I still am a little active in coaching. I do some private small-group lessons, so I stay connected. We still go to a lot of UH sporting events. Cheering on the men and women’s teams at UH is still a big part of our lives. And we travel a lot, mainly to see games.”

Here at home, the attention and passion Dave invests in his community includes advocating a balanced lifestyle for kūpuna, urging them to stay active and take care of their health. “Whenever I have a chance, I just like to encourage our generation to be healthy and stay active and exercise and eat well. I try to lead by example. When people see that I can still surf, and I’m golfing, and I’m exercising, maybe that will help get them off the couch.”

For the sake of helping others

Most of us have probably seen the Hawaii SHIP public service announcements (PSAs) while watching college sports on OC16. Dave sees it as a way to mentor a new age group: those in need of help navigating Medicare. “Vince mentioned he didn’t know a lot about what’s available and what help is out there, but I didn’t understand all of it either until I started taking these public service ads. I just think people like us, we gotta be kind of held by the hand now that almost everything is computerized and online. For some of us, it’s not easy. We didn’t grow up in this era,

so that’s one way that Vince and I have been able to help people.”

The two coaches became spokespeople chosen by Hawaii SHIP because of their reputations and familiar faces. “They had a very appealing proposition for Vince and I and Jim Leahey. We were all friends, we were all about the same age, and that made it attractive for us. Vince is probably the most humorous person I know, and they wanted something light and just pleasant to watch, not too serious.” Another part of the appeal was that “we were gonna be out at the stadium, or we were gonna be in the arena, or at some form of athletics we were known for.”

Goo on Shoji: He’s a year older than me, but that’s because he’s born in December and I’m January, so for a month, I can say, “OK, he’s older than me.” He can’t wait till that month goes by. He goes, “How old are you now?” Dave’s a cornerstone of our athletic department as far as wins are concerned, highlights, national championships. But, you know, he’s kind of on the serious side, yeah?

Shining a light for SHIP

Shining a light for SHIP

Both Dave Shoji and Vince Goo have remained active in terms of their physical health and their community for most of their lives. Today, the now-retired coaches can still be found participating in their respective sports, coaching private lessons or commentating for in-game analyses. Both of them treasure their “local boys” roots, as Dave puts it. He expresses his pride in growing up here, which is something both Dave and Vince share. Among other things, Dave and Vince also advocate for helping “their generation,” our kūpuna.

While they stress the importance of maintaining physical health as individuals age, they also encourage older folks to know what benefits they are eligible for and acknowledge the difficulties that come with navigating Medicare — especially for those who are not particularly tech-savvy. In our rapidly technologically advancing society, more help than ever is needed for those who face challenges in traversing websites, phone call prompts and more.

Medicare is one of multiple services where access to services can be hindered by complicated tech. Dave and Vince’s work with Hawaii SHIP has become an integral part of their activities in retirement, and the fun PSAs have proven to be quite a hit. “People go, ‘Oh, yeah, we saw your commercial!’ We had one that was animated but had our voices, and friends of mine went, ‘Oh, that’s the one you look best in,’” says Vince with a laugh. “But it has recognition, yeah? So, it’s serving its purpose.”

A different kind of game plan

In 2019, Lani Sakamoto, the supervisor for Hawaii SHIP, proposed to connect with Goo, Shoji, and Jim Leahey because all three individuals were Medicare beneficiaries by then. Sakamoto thought that a collaboration between Hawaii SHIP and the three men would prove incredibly valuable. Not only were they Medicare beneficiaries and utilizing the many services Hawaii SHIP provides, but the public’s recognition of three legends in the realm of UH sports would likely garner an overwhelmingly positive response.

Sakamoto then proposed the idea for some PSAs to the Spectrum cable company and to Kernel, a production company that had contact with the coaches because of the Spectrum’s channel, OC16.

Kernel took a low-key approach, “cobbling up” some scripts to guide the performance, but also letting the three friends act spontaneously and “play around” on camera. The key to each PSA’s appeal is how it conveys their natural sense of fun, while still addressing something important for audiences to know. Along with other helpful videos in several languages, the dynamic duo’s Spectrum PSAs can be viewed on the Hawaii SHIP YouTube channel here: youtube.com/@hawaiiship3802/videos

Braving unknown territory can be a daunting endeavor. In navigating the world of Medicare, the waters can prove to be especially rough and challenging. It also doesn’t help that there are some people and companies that would gladly take advantage of Medicare beneficiaries in need of healthcare services. With the right crew at your disposal, navigating Medicare can be smooth sailing — Hawaii SHIP (State Health Insurance Assistance Program) is here to guide you.

Braving unknown territory can be a daunting endeavor. In navigating the world of Medicare, the waters can prove to be especially rough and challenging. It also doesn’t help that there are some people and companies that would gladly take advantage of Medicare beneficiaries in need of healthcare services. With the right crew at your disposal, navigating Medicare can be smooth sailing — Hawaii SHIP (State Health Insurance Assistance Program) is here to guide you.

Hawaii SHIP is federally funded by the Administration for Community Living (ACL) and administered by the State Department of Health, Executive Office on Aging (EOA). Its mission is to empower, educate and assist Medicare-eligible individuals, their families, caregivers and soon-to-be retirees. Its volunteer-based program uses objective outreach, counseling and training to help those on Medicare make informed health insurance decisions that optimize their access to care and benefits.

Hawai‘i’s Medicare population is approaching 300,000, and Hawaii SHIP has counseled 2,765 clients and assisted folks numbering 6,465 through their outreach presentations and fairs.

For those who have difficulties with mobility or have vision impairment, their website also offers virtual presentations and resources in the form of podcasts/CDs as well as the option to request their resources in Braille.

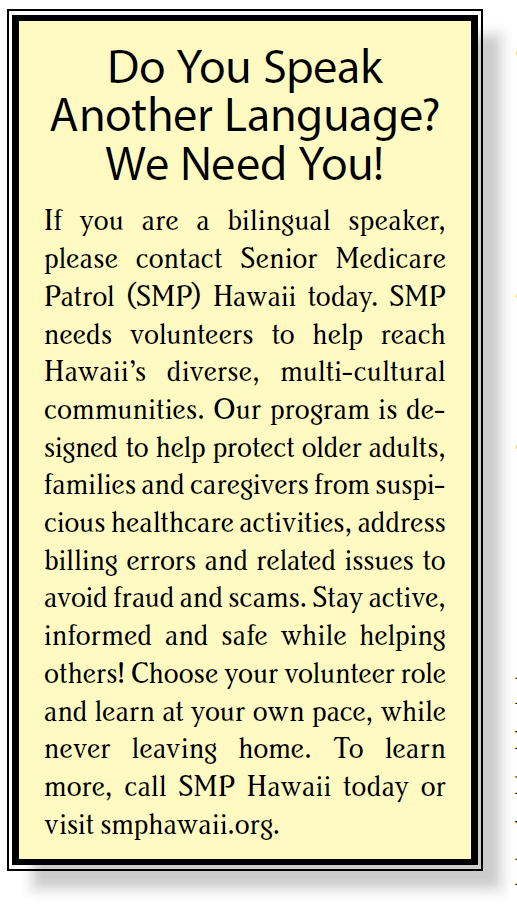

Once you contact Hawaii SHIP, you will be assigned to a certified volunteer counselor who will provide one-on-one guidance tailored to your specific situation and needs. These counselors help with understanding healthcare choices, matters of enrollment, plan comparisons, coverage and costs, prescriptions, troubleshooting billing issues, submitting appeals and referral to other possible resources. With your permission, Hawaii SHIP works directly with Medicare to resolve any issues on your behalf. Their SHIPMates are local community members who have undergone screening, training, and certification as Medicare experts. Hawaii SHIP has more than 80 SHIPMates. Recruitment for volunteers begins after Medicare’s Open Enrollment Period closes on Dec. 7.

Once you contact Hawaii SHIP, you will be assigned to a certified volunteer counselor who will provide one-on-one guidance tailored to your specific situation and needs. These counselors help with understanding healthcare choices, matters of enrollment, plan comparisons, coverage and costs, prescriptions, troubleshooting billing issues, submitting appeals and referral to other possible resources. With your permission, Hawaii SHIP works directly with Medicare to resolve any issues on your behalf. Their SHIPMates are local community members who have undergone screening, training, and certification as Medicare experts. Hawaii SHIP has more than 80 SHIPMates. Recruitment for volunteers begins after Medicare’s Open Enrollment Period closes on Dec. 7.

The benefits of volunteering with Hawaii SHIP include the joy derived from helping Medicare beneficiaries; learning about local support, services and resources; designing your own schedule and being able to choose a role suitable for you:

• Presenters educate community and employer groups about Medicare and other health plan options.

• Counselors provide assistance to beneficiaries, their families, caregivers and soon-to-be retirees.

• Exhibitors distribute educational materials at fairs and event booths.

• Administrative helpers support SHIP staff with various clerical duties such as data entry, making informational packets and translating materials into other languages.

• Information distributors transport brochures and newsletters about Hawaii SHIP and Medicare to sites where Medicare-eligible individuals gather (libraries, nonprofit agencies, community centers)

To become a SHIPMate or request help in your own journey, look to the lighthouse, a beacon in the dark — contact Hawaii SHIP today!

HAWAII SHIP

Free, local, one-on-one Medicare counseling is provided by the Hawai‘i State Health Insurance Assistance Program.

250 South Hotel St., Ste. 406, Honolulu, HI 96813

Oahu: 808-586-7299 | Toll free: 888-875-9229

hawaiiship.org/services | hawaiiship.org/volunteer

Medicare fraud is big business for criminals. Medicare loses approximately $60 billion annually due to fraud, errors and abuse.

Medicare fraud is big business for criminals. Medicare loses approximately $60 billion annually due to fraud, errors and abuse.